We are currently in the midst of increasing economic uncertainty and volatility. As a result, some analysts believe that some sectors of the economy may be approaching bubble territory. Inflationary pressures are rising, mortgages rates have increased significantly, housing affordability remains challenging for buyers, the stock market had previously reached record highs and current stock market valuations (even after the most recent correction) as measured by the cyclically adjusted price to earnings (CAPE) ratio remain high by historical standards. After years of boom/bust cycles, many financial analysts have developed signals that they believe are indicators of the potential for an upcoming recession.

So, what are some of the recession signals to watch for in the future?

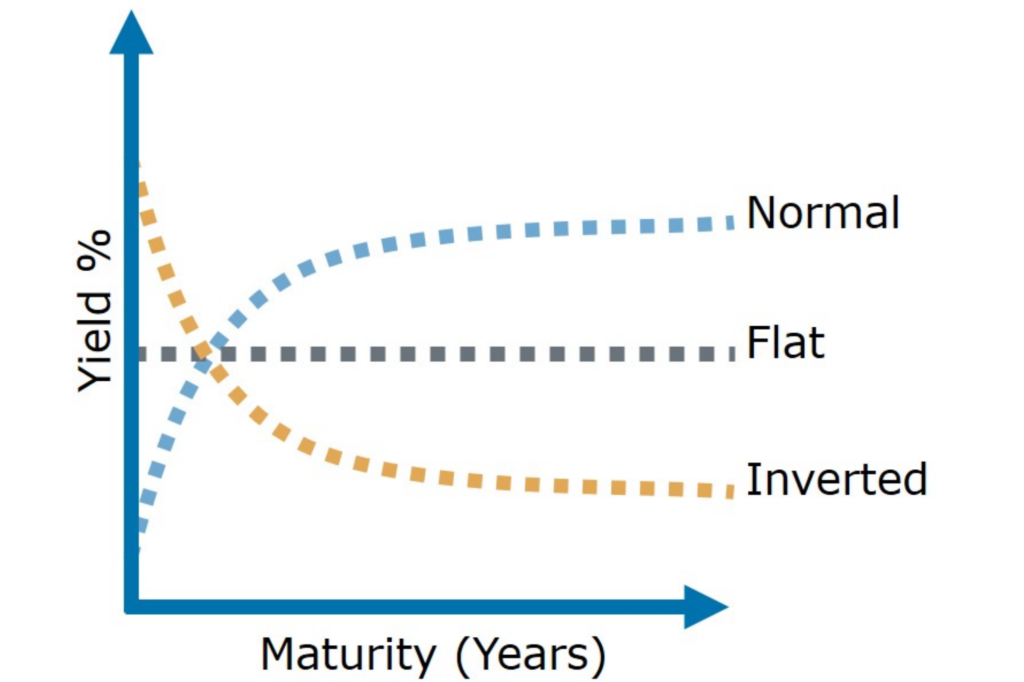

Yield-curve inversion

Yield-curve inversion

The yield curve is simply a graphical representation of the yield or interest rate on similarly rated bonds with varying maturities. The most commonly watched yield curve is the plotting of 3-month, 2 year, 5 year, 10 year, 20 year and 30 year government bonds. A normal yield curve is one where short-term bonds such as a 2-year bond would typically have a lower yield than a longer-term bond such as a 10-year bond. Generally, investors want to be rewarded for the greater risk associated with waiting a longer time period to be repaid for their principal. However, when the Federal Reserve raises short-term interest rates to combat inflation due to an over-heated economy, the yield curve can start to flatten or even invert. An inverted yield curve occurs when short-term bond yields are actually higher than long-term bonds.

Why does the yield curve matter? With the exception of a few cases, the yield curve has inverted before most recessions in history. While the yield curve has only partially inverted so far, some analysts believe that a few more rate hikes by the Fed could result in this occurrence.

An inverted yield curve is not a perfect signal as it does not guarantee recession and it may occur a year or two before recession - so it can be an early indicator. In fact, Ryan Detrick, senior market strategist at LPL Research, noted that during the past five recessions (not including the Pandemic), the market didn’t peak for more than 19 months on average after the yield curve inverted.

Leading Economic Index (LEI)

The Conference Board’s Leading Economic Indicators (LEI) is another tool used by many economists and analysts when assessing the likelihood of recession. Manufacturing new orders, initial applications for unemployment insurance, new building permits, stock prices and consumer sentiment are just a few of the 10 economic components that comprise the index and are often used to forecast the direction of future economic changes.

Why does the LEI matter? The longer-term trend in the LEI is especially important, as the index has turned negative year over year before every economic recession since the 1970s. While the LEI index is used by many analysts, it is also tends to be an early indictor. In fact, according to Putnam Investments, the LEI signal has historically had an average lead time of nearly six months.

How to prepare

While these are simply two of many economic indicators to watch, consistently predicting future movements in the economy or market are nearly impossible. Rather than attempt to “time the market”, it is important to focus on your “time in the market”. In particular, it may be a critical time in this cycle for investors to examine whether their portfolio remains in alignment with their goals, income needs and time horizon. When was the last time you assessed your risk or had a portfolio stress test? Do you have a time horizon that is long enough to allow sufficient time to account for future volatility? Is your portfolio in alignment with your life? Do you have sufficient cash reserves to help weather future economic storms? With interest rates rising, are your personal debt levels in manageable territory? Does your business have sufficient working capital and lines of credit in place?

Unfortunately, recessions do occur periodically over time. After all, economic expansions do not last forever. Since everyone’s situation is unique, consider speaking to your tax and financial advisers to determine the most appropriate financial planning approach for you.

Kurt J. Rossi, MBA, CFP®, AIF® is a CERTIFIED FINANCIAL PLANNER & Wealth Advisor. He can be reached for questions at 732-280-7550, kurt.rossi@Independentwm.com, www.bringyourfinancestolife.com & www.Independentwm.com. LPL Financial Member FINRA/SIPC.

{kind=link}