Now may be a great time to consider revisiting how you are investing your rainy-day fund. After years of holding short term interest rates at or near zero, the Federal Reserve has raised interest rates significantly this year. In an effort to subdue stubbornly high rates of inflation, many analysts believe that the Federal Funds rate will continue rising for months to come. Despite the fact that there are more online banks available and the Federal Reserve has just raised their benchmark interest rate to a range of 1.50 – 1.75 percent in June, the average American is still earning a paltry .10 percent APY on their savings. If you too are earning little to no interest on your cash reserves, it’s about time that you consider putting these important funds back to work.

An emergency cash reserve is a critical component of any balance sheet as it may help insulate you from the uncertainties in your financial life, especially recession risk. From the loss of a job and unexpected medical expenses to emergency repairs or even an investment opportunity, there is no shortage of financial what-ifs that people encounter over time.

Without proper reserves, unforeseen financial challenges often lead to debt. Remember, the single best strategy for combating debt is to prevent it in the first place.

Customize your reserves to your situation

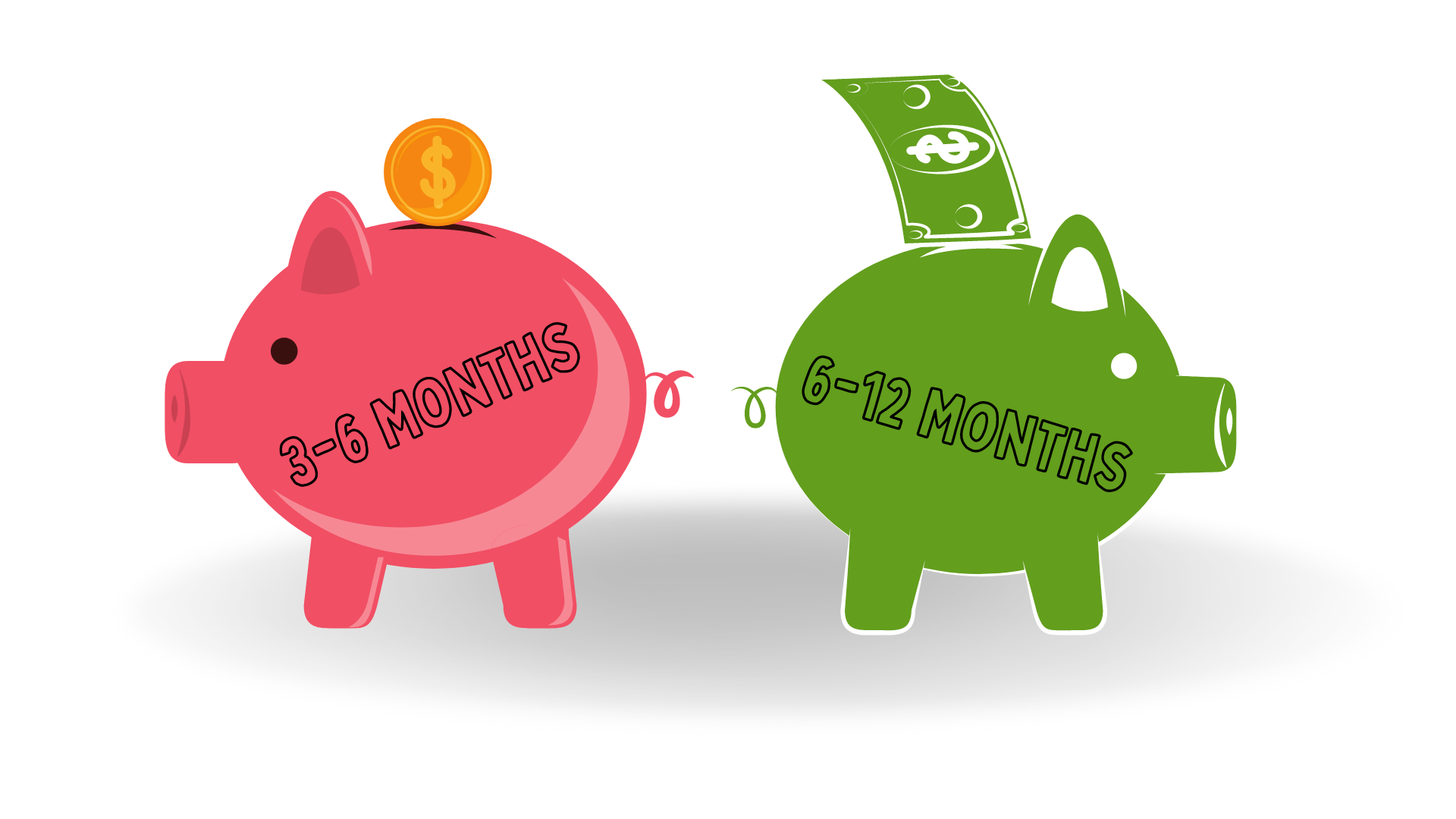

While most people agree that cash reserves are important, there are differing opinions on how much is necessary. More often than not, financial experts might suggest three to six months’ worth of liquid cash reserves. Others may suggest using a home equity line of credit for larger emergencies. While there are many different approaches, everyone’s circumstances are unique and the size of the optimal reserve needed will vary.

Generally, the more uncertainty in your financial life, the more risk you have and the larger the reserve you may want to consider. Households that rely on one income, larger families, those with insufficient health insurance coverage, and those working in trades with poor future job prospects are just a few examples of cases that may call for building relatively large reserves – possibly 6 to 12 months of expenses.

Assess your situation objectively, and if you determine that you fall into a high-risk category, consider building a larger safety net. Once you have determined the ideal size of your rainy-day fund, next it is time to put it to work.

Where to invest

When it comes to investing cash, boring is good. After all, cash reserves are not supposed to be exciting. Instead, a true cash reserve is generally going to be liquid, contain no risk and maintain FDIC insurance coverage.

Selecting the right bank

Selecting the right bank

There are a few important considerations when choosing the right institution for your reserves. The first one is obvious – what is the highest annual percentage yield (APY) that you can find? Rather than getting hooked by a “teaser rate” that will drop after an introductory period, it is important to work with institutions that are always competitive with their rates. Next, review minimum deposit requirements. Failing to meet minimums can lead to lower rates or maintenance fees so be careful here. Next, carefully review the fine print when it comes to withdrawals and transfers. Some institutions will limit transfer between accounts to only six transactions while other accounts may have other restrictions.

Should you lock up your money?

Locking up your money for longer periods of time may result in higher interest rates. The question you have to ask yourself is “am I being compensated enough for illiquidity?”. The answer is - it depends. If you believe that you may need to access the funds or that your high yield savings will keep up with future rate hikes (should they happen) there may not be a significant advantage to locking up your money for longer periods. Locking up your money for longer terms is generally advantageous if you believe future interest rates will be lower or if the rate difference is significant enough. While many analysts believe that the Fed may continue their plan of quantitative tightening, it is impossible to predict exactly what the Federal Reserve will do in the coming months. For this reason, a laddered approach with varied maturities can be appropriate in certain environments too.

For years, earning nearly no interest on your reserves was normal. Today, there are many more alternatives and it is possible that rates may move even higher. Since cash reserves are an important cornerstone to any sound financial plan, consider re-visiting your emergency fund. Since everyone’s situation is unique, consider speaking to your adviser to determine the most appropriate strategy for your needs.

Kurt J. Rossi, MBA, CFP®, AIF® is a CERTIFIED FINANCIAL PLANNER & Wealth Advisor. He can be reached for questions at 732-280-7550, kurt.rossi@Independentwm.com, www.bringyourfinancestolife.com & www.Independentwm.com. LPL Financial Member FINRA/SIPC.

{kind=link}